Definition

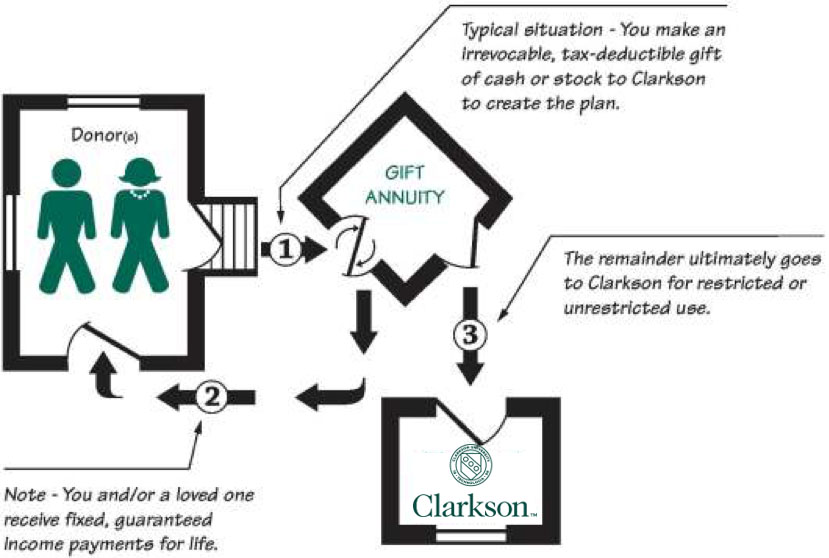

A Clarkson Charitable Gift Annuity is a contract between the donor(s) and Clarkson University that guarantees fixed payments to one or two income beneficiaries for life.

Further Information

A charitable gift annuity provides a fixed income for one or two lives, guaranteed by the assets of Clarkson University. Because the donor makes an irrevocable gift to create the annuity, some level of income tax charitable deduction may be generated in the year the gift is made. Clarkson University holds and invests all of your gift to generate income for your annuity payments. When the annuity terminates, Clarkson uses the remainder in the annuity for the purpose(s) designated when the annuity was created.

Annuity payout rates are determined by the age(s) of the annuitant(s), following the rate schedule recommended by the American Council on Gift Annuities (ACGA). Annuitants must be at least 50 years old when payments begin. The minimum amount to create a first annuity at Clarkson is $10,000. Additional annuities may be created. At the time the annuity is created, income payments may be arranged on a monthly, quarterly, semiannual or annual basis. Payments may be made by check or electronic deposit. A donor may not add future gifts to an existing annuity, but it is very easy to create another annuity, often at a higher payout rate. Gift annuities are most often funded with cash or publicly traded securities held long term (more than one year). In special circumstances, real estate may be used to fund a gift annuity. Under current law, grants from donor-advised funds may not be used to fund a gift annuity.

Changes to the Qualified Charitable Distribution (QCD) Rules

A QCD is a direct transfer of funds from your IRA, payable directly to charity. Amounts distributed as a QCD can be counted toward satisfying your RMD for the year, up to $100,000. The QCD is excluded from your taxable income, unlike with a regular withdrawal from an IRA, even if you use the money to make a charitable contribution later on. If you take a withdrawal, the funds would be counted as taxable income even if you later offset that income with charitable contributions. This could affect your tax brackets and phase out other benefits.

Gifts to create gift annuities may count in Clarkson fundraising campaigns, in your next anniversary reunion, and towards annual recognition. Contact the Annie Clarkson Society for help related to your unique circumstances.

Clarkson has invested its annuity assets with BNY Mellon Wealth Management, since 1999.

Create your own gift annuity projection with our gift-with-income calculator, or request a gift annuity projection by contacting the Annie Clarkson Society.

Request our workbook, Will a Gift-with-income Plan Work for Me?

Tax and Financial Implications

A donor may generally receive an income tax charitable deduction for some portion of the gift in the year that the annuity is created. The amount of the charitable deduction depends on the number and age(s) of the income beneficiaries and the IRS Discount Rate in effect at the time of the gift.

Assets grow within a gift annuity tax free. Income from a gift annuity is taxable. Depending on the type of asset used to create the annuity, the income stream may include some mix of ordinary, capital gain and tax-free income for the projected life of the annuity. If cash is used to fund the annuity, more of the income may be tax-free return of principal. If an appreciated security is used, more of the income may be capital gain. Income payments made past the projected life of the annuity will be taxed as ordinary income.

A gift annuity may be a good mechanism to convert a low yielding asset to a higher yield. A gift annuity may also be a tax-advantaged way to diversify a large block of a single stock without immediately declaring capital gain or to transition to a fixed-income position.

In general, if an appreciated asset, held long-term, is used to fund an annuity, the donor avoids paying capital gain on a portion of the appreciation. However, if income payments go to someone other than the donor and the donor’s spouse, the donor may be required to recognize all of the capital gain at the time the annuity is created.

If a donor wishes to use a depreciated security to fund an annuity, consideration should be given to selling the security first and then using the cash proceeds to create the annuity.

If an annuity makes income payments to someone other than the donor and/or the donor’s spouse, the donor may need to recognize a gift of the income payments to the income recipient(s). Careful planning may minimize any impact from this.

“Types” of Gift Annuities

Immediate payment gift annuity — This is the most common gift annuity, created for one or two lives. The donor is most often an income beneficiary. It is termed “immediate” because the first income payment is made within a year of the creation of the annuity. So, for example, if quarterly payments are selected, payments begin “immediately,” with the first payment made at the end of the quarter in which the annuity is created.

Deferred payment gift annuity — A donor may make a gift to create an annuity (and generate an immediate income tax charitable deduction), but delay the start of income payments until some time in the future (at least one year from the creation of the annuity). The beginning date of payments is defined in the annuity agreement. The longer the deferral period, the higher the payout rate when payments begin. The income recipient(s) must be at least 50 years old when payments begin. Deferred gift annuities are often used to plan retirement income, or simply generate a higher payout rate by waiting for payments to begin.

Flexible gift annuity– This is a deferred gift annuity that includes in the agreement a schedule of elective payment start dates and the corresponding payment amounts. The donor may later select a start date from the schedule in the agreement. Unlike a deferred gift annuity, however, the amount of the income tax charitable deduction is determined by the date of the gift, not the date that income payments begin.

Income for someone else — This gift annuity provides income for someone other than you or your spouse. It can be a creative way to make a gift to Clarkson and also provide fixed income to a parent, sibling or other loved one. Generally, an income tax charitable deduction is generated for the donor at the time the annuity is created. The donor must be careful, however, in deciding which asset should fund the annuity, and what level of income to provide to the beneficiary. If appreciated stock is used to fund the annuity, the donor may be required to declare some or all of the capital gain on the stock. Also, the income payments are considered a “gift” from the donor to the beneficiary, so gift tax may be an issue as well. With careful planning, problems can be avoided. Income payments are taxable to income beneficiaries, usually at ordinary income rates.

Testamentary gift annuity — A testamentary gift annuity is a way to provide a fixed income stream to a sibling, relative, caregiver or other loved one. This gift annuity is created through language in your will or living trust to provide income to an heir at the time your estate is settled. The payout rate and any tax benefits are determined at the time the annuity is created by your estate. The remainder is used by Clarkson when the annuity terminates.

Commuted payment gift annuity — This is a deferred annuity that includes an option for the income beneficiary to exchange his/her lifetime payments for a fixed number of payments. Often termed a “college” or “tuition assistance” annuity when created to make payments to a student attending college. Note: New York State law prohibits charities located in NYS from creating commuted payment gift annuities.

Charitable Gift Annuity Rates

The American Council on Gift Annuities (ACGA) has recommended gift annuity rate schedules since 1927. When a charitable gift annuity is funded, the age-appropriate rate from the schedule determines an annual amount paid to the income beneficiary that never changes and is guaranteed by Clarkson for the life of the annuitant(s). Most charities, including Clarkson, voluntarily adopt ACGA rate schedules to eliminate competition and ensure that gift annuities remain charitable vehicles that offer an income tax deduction.

The ACGA board of directors recommended a new rate schedule effective January 1, 2023. Click here for a review of the rates and the assumptions behind the ACGA rate schedule.

The charts below list payout rates for 1-life and 2-life immediate payment gift annuities. Deferred payment gift annuity rates are dependent on the age(s) of the beneficiary(ies) and the length of the deferral period (at least one year). You may calculate a deferred gift annuity rate on our gift-with-income calculator.

For help with questions, contact Annie Clarkson Society, or call toll-free 877-928-4438.

To learn more about charitable gift annuities, request our workbook, Will a Gift-with-income Plan Work for Me?

Gifts to create gift annuities may count in Clarkson fundraising campaigns, in your next anniversary reunion, and towards annual recognition. Contact the Annie Clarkson Society for help related to your unique circumstances.

Process to Create

While every gift situation is unique, there are several steps that may be outlined to help clarify the process. When an individual creates a gift annuity at Clarkson, he/she will most likely follow steps similar to the ones below. The process often begins with a conversation:

- We talk. An initial conversation with the Annie Clarkson Society is advisable to help the University understand your priorities and goals and determine which plan(s) may best fit your needs. The Annie Society will then prepare a proposal for your review.

- You review. The proposal will include a financial projection with explanations and background information for review by you and your advisors. Additional information or further projections may be required to answer questions and clarify the exact benefits and circumstances that will be right for you.

- You decide. Once all of the information is presented and reviewed, it is time to decide if the timing and circumstances are right to proceed and create your gift annuity.

- You arrange transfer. At this point you write the check, authorize transfer of the stock, or otherwise arrange for ownership of the asset(s) to pass to the Clarkson gift annuity account. Once ownership of the asset passes to the account, the University determines the gift date and the value of the gift. (It’s easy with cash, but gets more complicated with multiple transfers of stock, for example). That data then allows the office to prepare final calculations and a gift annuity agreement.

- You sign. Final materials and agreements are sent for signature, along with a gift receipt. At this point the Annie Society will arrange the method for future payments. The office will also wish to make sure the University has documented your wishes for the final use of your gift at Clarkson.

- You relax, payments begin. Unless payments are deferred, the first payment is made at the end of the period as established by the annuity agreement. A first payment may be a partial payment, depending on the date of the gift. The Annie Society will also contact you to ensure that the first payment was processed correctly.

What

to Expect After Your Plan is Created

The creation of your gift annuity is the start of a new relationship with

Clarkson:

- If you are a new member of the Annie Clarkson Society, you will receive letters of welcome.

- At the end of each payment period, you will receive either your check, or a “cash advice” of your electronic payment directly from BNY Mellon Wealth Management through their Boston offices.

- You will receive an annual financial report from the Annie Society each January.

- 1099R income tax statements will be mailed to you directly from BNY Mellon by January 31 each year.

- As an Annie Clarkson Society member, you will receive the society newsletters and annual report each year.

- Clarkson asks that income beneficiaries report to the Annie Society any change in address or bank account information as soon as possible, so that there is no interruption in the processing and receipt of income payments.

You can contact the Annie Clarkson Society at 315-268-7894 or e-mail AnnieSociety@clarkson.edu for further information.

This web page does not provide legal or financial advice, nor is it a comprehensive review of the topic. You should consult your legal and financial advisors and Clarkson University before making or planning your gift.