Definition

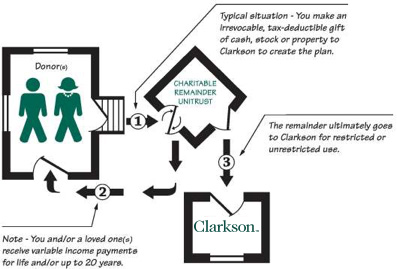

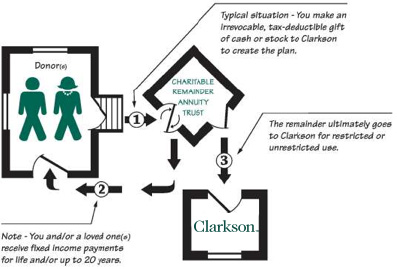

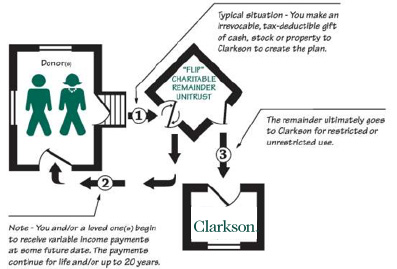

A charitable remainder trust is a separate legal entity created to hold and invest assets that will ultimately pass to Clarkson. Income from the investment of the assets is paid to a beneficiary or beneficiaries for life (lives) and/or a period of up to 20 years.

Further Information

A trustee is named at the creation of the trust and is responsible for the management of the trust. If Clarkson is to be named trustee, the University will provide a draft trust document for review by the donor and the donor’s advisors.

A charitable trust is an irrevocable gift vehicle, and the remainder in the trust must pass to charity when the trust terminates. Because a gift to the trust is irrevocable, the federal government allows an income tax charitable deduction for some portion of the gift, determined by factors at the time the asset is transferred into the trust. The minimum amount to create a trust at Clarkson is $25,000. Income beneficiaries must be at least 50 years old when payments begin.

The trust payout percentage is stated in the trust document and cannot change. By law, the percentage must be no less than 5%, (most Clarkson trusts are in the 5-6% range). Although most trusts run for one or two lives, it is possible to create a trust for more than two lives. It is also possible to create a trust for a set period of years, up to 20. Payments to income beneficiaries must be made at least annually from the trust, and payments are guaranteed based on the availability of assets within the trust.

It is possible to fund a trust with non-cash assets such as real estate. In a typical case, a “Flip-CRUT” is created (see below), the real estate is donated to the trust, and the trust begins making payments to beneficiaries at some point after the real estate is sold and the proceeds re-invested.

Under current law, grants from donor-advised funds may be used to fund a charitable trust.

Secure Act 2.0 Allows the Use of QCDs to Establish Gifts with Income

Beginning in 2023, donors over age 70½ or older, may elect as part of a QCD a one-time gift up to $50,000 (per individual), to establish a charitable remainder unitrust, a charitable remainder annuity trust, or a charitable gift annuity. This amount counts toward the annual RMD. Note that for gifts to count, they must come directly from your IRA by the end of the calendar year.

Income payments may be made annually, semiannually, quarterly or even monthly. Payments may be mailed or deposited electronically to a bank account. Clarkson trust assets are invested through BNY Mellon Wealth Management.

Gifts to charitable trusts may count in Clarkson fundraising campaigns, in your next anniversary reunion, and towards annual recognition. Contact the Annie Clarkson Society for help related to your unique circumstances.

Income for someone else: Trusts are often used to provide income for someone other than the donor or the donor’s spouse. It can be a creative way to make a gift to Clarkson and also provide income to a parent, sibling or other loved one. Generally, an income tax charitable deduction is generated for the donor at the time the trust is funded. The donor must be careful, however, in deciding what asset should fund the trust, and what level of income to provide to the beneficiary. If an appreciated asset is used to fund the trust, the donor may be required to declare some or all of the capital gain on the asset. Also, the income payments are considered a “gift” from the donor to the beneficiary, so gift tax may be an issue as well. Careful planning can help avoid problems.

Deferred income payments: You may defer the start of income payments for any period of time with a “flip unitrust.” The deferral period must be defined in the trust document, and the “flip event” must be out of the control of the donor (e.g., a birthdate or calendar date). Assets grow tax-free during the deferral period. Once income payments begin, they cannot be stopped.

Testamentary trusts: One gift and estate planning technique is to create a trust through your estate plan to provide income for heirs before passing the remainder to Clarkson. It is important to discuss this option with your gift planning and legal advisors to structure the trust correctly and make sure the plan will meet your intentions.

Are you thinking of funding a charitable trust at Clarkson and would like to speak confidentially to someone who already has a trust? Tom Basso ’74 would be happy to hear from you. Email Tom at tombasso@clarksonalumni.com.

Create your own charitable trust projection with our gift-with-income calculator or request a charitable trust projection from Clarkson.

Request our workbook, Will a Gift-with-income Plan Work for Me?

Tax and Financial Implications

The age(s) of the income beneficiary(ies), the percentage payout rate, and to a lesser extent, the IRS discount rate at the time the trust is funded determine the amount of the income tax charitable deduction. The donor must take the deduction for the tax year in which the trust is funded, up to a maximum amount allowable based on the gift asset and the donor’s adjusted gross income. Any excess deductible amount may be carried forward for up to five additional years.

If a trust is funded with an appreciated asset (held long term), in most cases the donor will not need to declare any capital gain on that asset at the time of the gift.

Assets within the trust grow tax free. Trust payments to income beneficiaries are taxable income. Depending on the investment performance of the trust, income payments may be a mixture of ordinary, capital gain and, to a lesser extent, tax-free income.

While projections can be created, the actual remainder value to Clarkson will depend on the market performance over the life of the trust, the payout percentage and how long the trust makes payments to beneficiaries. Projecting the remainder value may be of particular interest to a donor who, for example, wishes to create an endowed fund at the University at a certain level with the remainder from the trust.

The assets in a trust may be included in a donor’s estate. But when the remainder passes at death to Clarkson, it is fully deductible, resulting in no net estate tax liability.

“Types” of Charitable Remainder Trusts

There are several types of charitable remainder trusts. By far, the most common is a charitable remainder unitrust (CRUT or STANCRUT for “standard unitrust”), where annual payments are based on a set percentage of the assets of the trust, revalued once each year. This means that income payments will vary year to year based on the investment performance of the trust. Additional tax-deductible gifts may be made to an existing unitrust at any time.

Another type of trust, a charitable remainder annuity trust (CRAT), determines a payout dollar amount when the trust is created, and that amount never changes, as long as there are assets in the trust to make payments. Additional future gifts may not be added to an annuity trust after it is initially funded.

A hypothetical comparison of a unitrust and an annuity trust payout over several years might include:

| Year | Annual Revaluation | Unitrust (CRUT) Payout at 5% | Annuity Trust (CRAT) Payout at 5% |

|---|---|---|---|

| 1 | $100,000 | $5,000 | $5,000 |

| 2 | $103,000 | $5,150 | $5,000 |

| 3 | $99,000 | $4,950 | $5,000 |

| 4 | $102,000 | $5,100 | $5,000 |

A net income unitrust (NiCRUT) is generally defined to make payments only from the income (not capital appreciation) to the trust each year, up to the required percentage payout amount. If income is not sufficient, then the full amount is not paid out in that year. A net income with make-up unitrust (NiMCRUT) allows unpaid amounts from previous years to be made in subsequent years if income is sufficient.

A Flip Unitrust (Flip CRUT) is often used when non-cash or hard to value assets are gifted to a trust, or when a donor wishes to defer the start of income payments from the trust. The trust starts out as a net income trust (see above). A “triggering event” “flips” the trust from a net income to a standard unitrust. The “triggering event” to start the flow of income must be defined within the trust document and must be out of the control of the donor. For example, selling a home donated to the trust or reaching a 65th birthday may be out of the donor’s control, but the date of sale of a publicly traded stock is most likely within the control of the donor. As with all charitable trusts, once income payments begin, they cannot be stopped.

Process to Create

While every gift situation is unique, there are several steps that may be outlined to help clarify the process. When an individual creates a charitable trust at Clarkson, he/she will most likely follow steps similar to the ones below. The process often begins with a conversation:

- We talk. An initial conversation with the Annie Clarkson Society is advisable to help the University understand your priorities and goals and determine which plan(s) may best fit your needs. The Annie Society will then prepare a proposal for review by you and your advisors.

- You review. The proposal will include a financial projection with explanations and background information on the trust for review by you and your advisors. Additional information or further projections may be required to answer questions and clarify the exact benefits and circumstances of a trust that will be right for you.

- You decide. Once all of the information is presented and reviewed, it is time for you to decide if the timing and circumstances are right to proceed and create a trust. If Clarkson will be the trustee, the University will prepare a tailored draft trust document for review and signature.

- You arrange transfer. At this point you write the check, authorize transfer of the stock, or otherwise arrange for ownership of the asset(s) to pass to the charitable trust. Once ownership of the asset passes to the trust, the University determines the gift date and the value of the gift. (It’s easier with cash, but gets more complicated with multiple transfers of stock, for example). That data then allows the office to prepare final financial calculations. At this point the Annie Society will arrange the method for future payments from the trust. The office will also wish to make sure the University has documented your wishes for the final use of your gift at Clarkson.

- You relax, payments begin. Unless payments are deferred, the first payment is made at the end of the period as established by the plan, (e.g., the end of the quarter). A first payment may be a partial payment, depending on the date of the gift. The Annie Society will also contact you to ensure that the first payment was processed correctly.

What to Expect After Your Plan is Created

- The creation of your plan is the start of a new relationship with Clarkson: If you are a new member of the Annie Clarkson Society, you will receive letters of welcome.

- At the end of each payment period, you will receive either your check, or a “cash advice” of your electronic payment directly from BNY Mellon Wealth Management through their Boston offices.

- Trust beneficiaries receive a financial report of their trust each June from BNY Mellon.

- Trust beneficiaries (of variable payment trusts) will receive an annual letter from BNY Mellon including the re-valuation figure for the trust and the amounts of income payments for the coming year.

- Trust beneficiaries receive a financial report from the Annie Society each January.

- K1 income tax statements to trust beneficiaries are targeted for mailing from BNY Mellon by February 28 each year.

- As an Annie Clarkson Society member, you will receive the society newsletters and annual report each year.

- Clarkson asks that income beneficiaries report to the Annie Society any change in address or bank account information as soon as possible so that there is no interruption in the processing and receipt of income payments.

You can contact the Annie Clarkson Society for more information.

Follow us on Twitter @annieclarkson

This web page does not provide legal or financial advice, nor is it a comprehensive review of the topic. You should consult your legal and financial advisors and Clarkson University before making or planning your gift.